A good financial plan creates a roadmap or a guiding light for your financial life journey. It’s more than money and gives you an overall picture of where you stand financially and where you’re heading to. It should include financial details about your cash flow, savings, debts, investments, insurance, and any other aspects of your finances.

Financial planning is an ongoing process that allows you to get your money and life under control so that you can reduce stress, fear, and worries about your future life. I think everyone should have one, and it can be done in your own style or with a financial planner. Remember, financial planning is not only for the wealthy or people earning a high income.

You don’t need sophisticated software or tools to draw up your own financial plan; instead a blank piece of paper will help you to kick start the process. Start by listing down what you have (assets eg. savings account, EPF, investment account, investment property, business, etc.) and what you owe (liabilities eg. mortgage loan, car loan, personal loan, credit card, study loan, etc.), income (cash inflow) and expenses (cash outflow). This will give you a snapshot of whether you’re at a financial surplus or deficit, making it easier to work out a financial plan – covered in the next step.

Setting goals for your financial plan

This is where you decide how to design your own life. When crafting your own financial plan from the viewpoint of what your money can do for you, you’ll make saving and investing feel more intentional than overspending it. Your goals should be inspirational, measurable, and realistic – ask yourself where do you see yourself in five years’, 10 years’ or even 20 years’ time? It’s important because it gives you direction to achieve your financial goals at different life stages and it also influences how you plan your career as well.

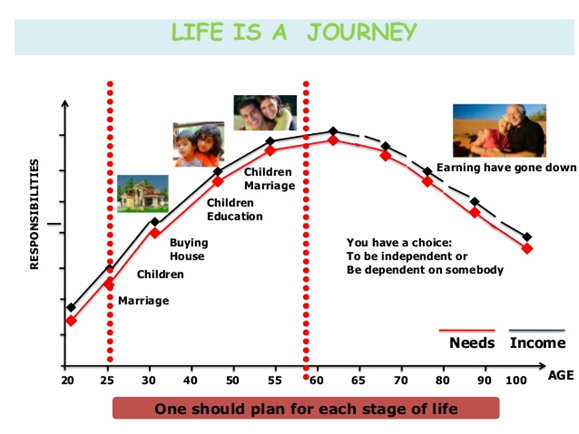

For example, there will be different needs when doing financial planning in your 20s, 30s, 40s and 50s. In your 20s, you might want to make sure you have sufficient emergency savings that lasts for at least three to six months so that in emergencies you won’t be running on credit. Don’t forget to factor in insurance and ensure you get adequate coverage for personal accidents and a medical plan.

In your 30s to 50s, you’ll likely be experiencing high commitments due to getting married, raising kids, preparing university tuition fees, and funding your retirement fund. As you progress from different life stages, you’ll need to regularly keep an eye on your allocations for investing and spending. If you know that these things will happen in your 30s to 50s, you may save and invest more in your 20s or prolong the retirement age from 55 to 60.

Monthly budgeting for your financial plan

The next step is to allocate your monthly budgeting – what is coming in and what is going out to understand your spending habits and only able to take a balance between spending and savings. It depends on where you live and how you spend – living in an urban area may result in spending more due to higher rent, eating out more etc. If you don’t spend more than half of your income, then you can start saving enough to fund your goals. Of course, you can’t own the whole world, but you can own the things that you value the most!

Executing your financial plan

This is all about allocating your resources or cash surplus to fund your goals. Saving and investing must come into play and you should consider the types of financial products, the risks, returns and liquidity, as well as understanding your risk tolerance. For example, if you set aside 15% of your gross income for long-term goals like retirement, you may consider investing in stocks or equity funds that aim for capital appreciation. For shorter goals like saving for an emergency fund, you wouldn’t put your money in a high-risk fund because you might need it quickly in an emergency. It’s best to have separate accounts for different funding purposes.

Review your financial plan

Lastly, review and monitor your financial plan regularly to ensure you exercise strict discipline with the flexibility to adjust accordingly in the future, especially when entering different life stages. It’s easy to talk and plan, but execution remains the most challenging task as we may not have the discipline to stay on track. So, reviewing, monitoring and fine-tuning acts as reminders of your goals all the time. It’s best if you can make it measurable so that you can reward yourself with small gift when you are on track!

A good financial plan is not a beautifully written document that is presented nicely to you. It’s a tool to track your progress and help you reevaluate plans after a life milestone such as getting married, raising a kid, buying your first property, upgrading to a new car, preparing for a kid’s college fee, or building your retirement fund. When everything is handled, you can enjoy living your life. The small steps you are taking now will definitely have a huge, positive impact on your future.

About the author

Eewen is a licensed financial planner and strongly upholds the belief that financial wellness is all about money bringing a positive impact into your life. She can be contacted at keaheewen@vka.com.my

Content retrieved from: https://www.smartinvestor.com.my/how-to-make-a-financial-plan-beginner/.